First Sale for Export (FSFE) is a duty reduction program designed to reduce the dutiable value of eligible products imported into the United States.

With the increased tariffs of 2025 in mind including IEEPA and Section 232, in addition to Section 301, AD/CVD, etc., FSFE is a valuable duty mitigation strategy for importers with qualifying transactions to mitigate tariff impacts.

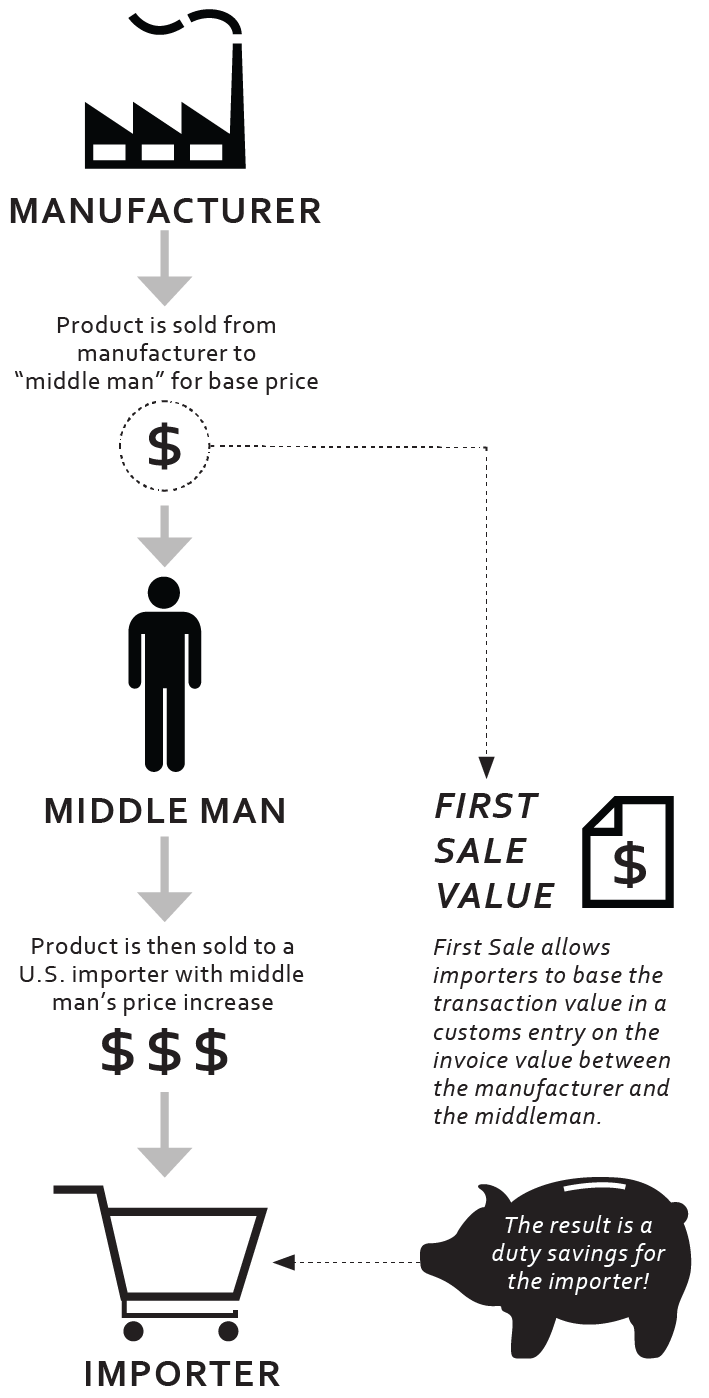

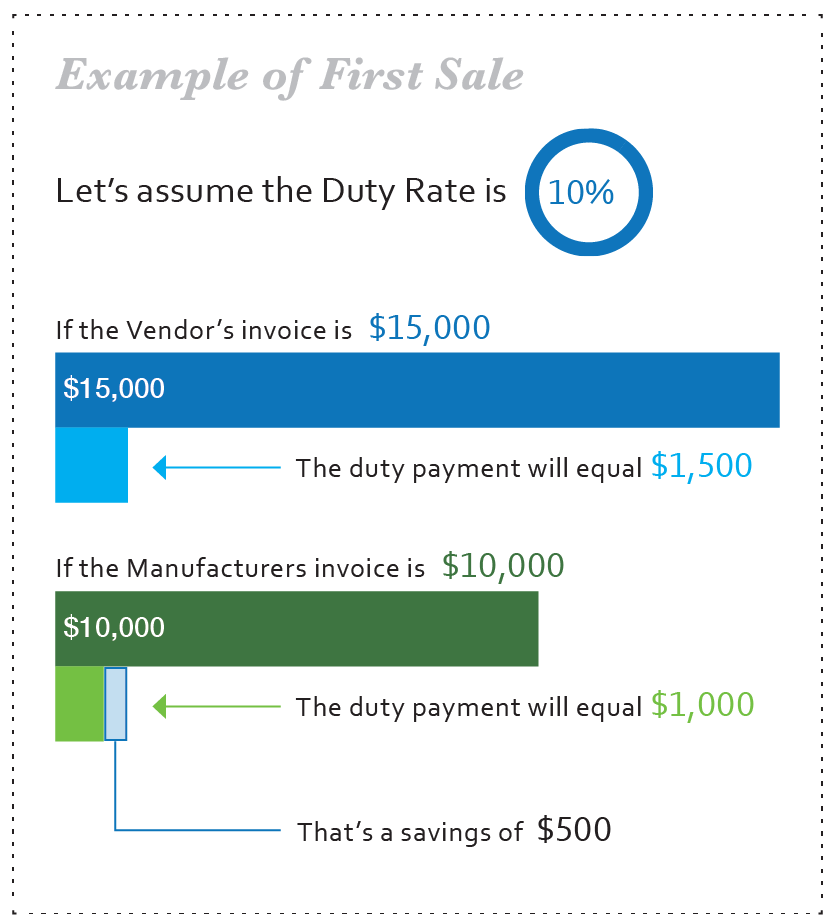

Normally when goods are imported into the U.S., duty is based on the value of the goods when purchased by the importer. This means that if a multi-tiered transaction exists, where a manufacturer sells to a middleman who in turn marks up the price and then sells the goods to the importer, the importer would be paying duty based the “Second Sale”, or the middleman’s value, which includes the middleman’s profit.

FSFE valuation establishes the dutiable value of the merchandise based on the “First Sale” between the manufacturer and the middleman. This excludes the middleman’s markup, thereby lowering the duties payable and resulting in potentially significant savings.

Who is a Candidate for First Sale?

Historically, FSFE valuation has been principally used by apparel and footwear retailers with high volume imports and relatively high duty rates. However, any importer bringing goods into the U.S. using a “multi-tiered” transaction model may be eligible for FSFE valuation.

In today’s trade environment, with historically high duty rates, companies in every industry are reviewing if a First Sale for Export program is right for them.

Tradewin's Approach

Tradewin's valuation experts have prepared an integrated methodology designed to ensure the proper application of this valuable duty reduction method. Our unique approach covers the full range of issues that have previously caused importers to shy away from FSFE valuation.

Our methodology includes a thorough review of the client's import activity to identify First Sale opportunities, an introduction of the program to our client's supply chain partners, and preparation of case studies specifically designed to address the importer's unique circumstances. This process is designed to meet all of CBP's stringent reasonable care requirements.

Our case study methodology tests the key tenets of First Sale to ensure that transactions are structured to successfully leverage the program. These include the following requirements.

Requirements for First Sale for Export Valuation

- Arm’s length transaction – The importer must be able to prove through documentation that an “arm’s length” transaction occurred, meaning that the price between the middleman and the manufacturer was negotiated free of influence by the relationship.

- Clearly destined for export to the U.S. – At the time of purchase order from the importer through the financial and physical flow of goods, it must be clear that the goods are destined for the U.S.

- Bona fide sale for export – The importer must establish that there are two separate transactions occurring between (1) the importer and the middleman, and (2) the middleman and the manufacturer. Transaction structure must establish that the vendor takes risk of loss for the product and does not act as a buying or selling agent.

- All dutiable costs declared – The total value will include all statutory additions to price, including any applicable packing costs, commissions, assists, or royalties/license fees related to the imported merchandise.

Our Results

Utilizing the First Sale for Export program, Tradewin has successfully helped our customers save millions in duties owed to CBP. That number continues to grow as more and more importers understand the significant impact a First Sale program can have on their bottom line.

An FSFE program can be advantageous in various industries including electronics, automotive, and retail, to name a few. Please contact Tradewin today to learn more about this valuable program. We are here to help.